A freehold address, in one of Singapore’s most central industrial districts, on the cusp of a JTC-led rejuvenation. The conditions for this kind of opportunity rarely converge — and when they do, they tend to close quickly.

In Singapore, the most consequential real estate decisions are usually about what you cannot get back once it is gone. Freehold land is the clearest example. Central location is another. And every so often, a third factor — a planned upgrade of the surrounding district — quietly resets the long-term value of an address that was already attractive to begin with.

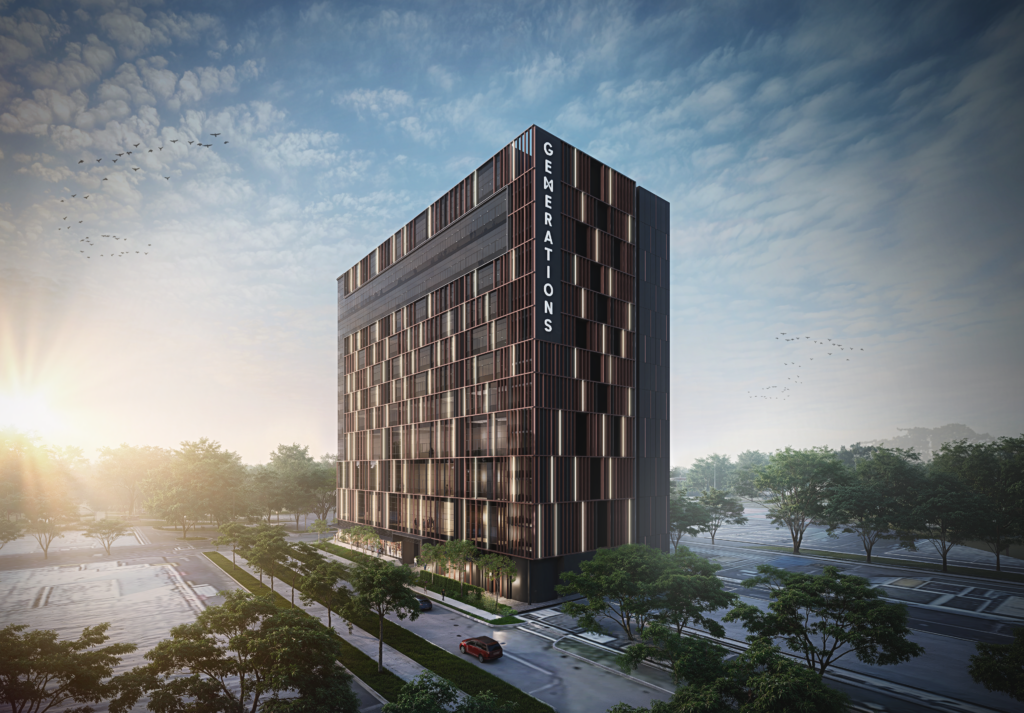

Generations @ Tannery sits where all three of those things meet. It is one of the rare new freehold B1 industrial buildings being built in central Singapore, in a district that is already well-served, and that the government has explicitly identified for the next phase of industrial-estate transformation.

We do not say this lightly. We have looked at every directly comparable freehold strata industrial launch in the last several quarters. This one is unusual.

“Freehold. Central. Inside a district being upgraded. Three rare conditions in one address.”

1. Freehold Industrial Is Becoming a Vanishing Category

The vast majority of industrial land in Singapore — over 80 per cent — is held on JTC leases of 30 or 60 years. New industrial sites released through Government Land Sales are almost without exception leasehold. Freehold industrial buildings exist, but most date from earlier decades and trade tightly held when they trade at all.

This matters for two reasons.

Tenure controls long-term value. A 30-year lease that is fifteen years into its life is, in capital terms, a depreciating asset on a defined runway. A freehold title is not. Over a hold period long enough to matter — ten, fifteen, twenty years — the gap compounds in directions that are often underestimated at purchase.

Replacement supply is structurally constrained. Because new freehold industrial supply is effectively zero, the existing stock is a closed pool. Each new freehold building that comes to market in central Singapore is, in a real sense, an addition to a category that does not naturally grow.

For investors who think in terms of capital decisions rather than transactions, this is the single most important characteristic of the asset.

2. A Central Address — Not in Name Only

“Central” is a word that gets stretched in Singapore property marketing. In this case, the location does the work without help.

71 Tannery Lane sits in District 13, inside the MacPherson / Aljunied / Geylang precinct — historically one of the city’s most established light-industrial belts, and one of the few that combines genuine logistics infrastructure with residential and commercial density.

Practically:

Five minutes’ walk to Mattar MRT on the Downtown Line — meaningful for staff retention, client visits, and tenant economics. Walkable MRT access is the single biggest differentiator we see in industrial occupancy data.

Direct connectivity to three major expressways. PIE, CTE and KPE are all within minutes by vehicle. For occupiers running goods movement, supplier logistics, or distribution, this is not a marketing claim — it shows up directly in operating cost.

Inside the existing demand catchment. The area is already home to a deep base of light-manufacturing, e-commerce, logistics, and creative-industry tenants. Vacancy at well-specified buildings in this corridor has been consistently below the broader market average.

You do not have to model this. You can stand on the road and see it.

3. The Kallang–Kolam Ayer Transformation Is Already Underway

This is the part most buyers under-weight, because it requires looking five to ten years ahead.

The Kallang–Kolam Ayer industrial estate is one of two mature industrial districts that JTC and URA have explicitly identified for sustainable rejuvenation, alongside Yishun. The framework has been progressing since 2020 and is now actively reflected in the URA Draft Master Plan 2025.

The direction of travel is consistent across multiple official touchpoints:

Mixed-use intensification. “Transparent factories” — open, ground-floor industrial spaces with public-facing showrooms — alongside co-working space and lifestyle amenities. The intent is to integrate industrial and non-industrial uses in a way that has not previously been done at scale in Singapore.

Connectivity upgrades. The Kallang Park Connector — a 10-kilometre trail running from Bishan to the CBD, with a 682-metre bridge over the PIE planned for completion by 2027 — runs through the broader catchment. The Thomson-Kallang Corridor adds homes, workplaces and public space along the Kallang River.

MRT integration. The masterplan framework references seven MRT stations within walking distance of the broader district once phased upgrades complete. Pedestrian bridges and improved walking and cycling routes are being designed in.

“You are not just buying an address today. You are buying that address while the district around it is rebuilt.”

The translation, for an investor: you are not just buying an address today. You are buying that address while the district around it is rebuilt to be denser, more amenity-rich, more accessible, and more mixed-use than it is today. Surrounding-area transformation of this kind has historically been one of the most reliable supports for long-term capital values in Singapore.

What Just Happened Next Door

We do not normally use a single recent transaction to make a point. In this case the precedent is too direct to ignore.

Just a few weeks ago at the beginning of May 2026, CT Gold — a freehold ramp-up B1 industrial development on Lorong Bakar Batu in MacPherson, in the same district as Generations and built to the same general format — was launched. It sold out in two days.

The detail that matters: the buyers were predominantly multi-unit buyers, taking two to four units each. Single-unit buyers who arrived without a pre-launch position largely walked away empty-handed.

That is not a marketing line. It is a description of the demand pattern that exists, right now, for this exact product type in this exact micro-market. New freehold B1 supply meets organised, repeat-buyer capital — and the supply clears immediately.

When the same product type comes to market in the same district two months later, it is reasonable to expect the same pattern to repeat. Possibly more so, given that the next launch sits inside the rejuvenation footprint and is closer to a Downtown Line MRT.

The Interest-Rate Window Is Open Today

There is one further factor that may not stay favourable indefinitely. The current interest-rate environment is materially below where it was even eighteen months ago. For an asset class where most buyers carry significant leverage, the cost of debt directly determines what a buyer can afford to pay and how the underlying economics work.

Lower rates do two things at the same time. They reduce the carry on a financed position, which makes the holding period more comfortable. And they raise the price that the same level of equity can support, which means the addressable buyer pool is wider while rates remain low.

Neither of those effects is permanent. Rate environments move. Windows open and close. The buyers who position themselves while conditions are favourable are typically the ones who look back, three or five years later, and find they made the easier decision.

“The conditions are not always going to be this lined up at the same time.”

Why We Are Flagging This One

Bluewater Group does not market launches that do not pass our own analysis. Most do not. We focus on a small number that combine genuine investment merit with conditions that are not easily reproduced.

This project meets that test. It combines:

A freehold tenure in a category that almost never sees new supply.

A central, MRT-served address in a district with established occupier demand.

Inclusion in a long-dated, government-led rejuvenation framework that is already in motion.

A directly comparable launch nearby that demonstrated, two months ago, exactly what happens when a product like this comes to market.

A financing environment that — for now — supports the asset’s economics in a way that cannot be assumed to last.

The conditions are not always going to be this lined up at the same time. For investors and business owners who have been waiting for a freehold industrial entry in central Singapore on terms that make long-term sense, this is the window we would not let pass without a closer look.

Have a Closer Look — At the VVIP Preview

We are happy to walk you through the project, the comparable analysis, and the financial framework on a no-obligation basis. The VVIP Preview is on now until July 15th.

Bluewater Group — Real estate advisory with banking-grade discipline.

Leave a Reply